The unified tax credit gives a set dollar amount that an individual can gift during their lifetime before any estate or gift taxes apply. The tax credit unifies both the gift and estate taxes into one tax system which decreases the tax bill of the individual or estate, dollar to dollar.

Who will pay estate tax Philippines?

The estate tax imposed is generally paid by the executor or administrator before the delivery of the distributive share in the inheritance to any heir or beneficiary. Where there are two or more executors or administrators, all of them are severally liable for the payment of the tax.

How can I avoid paying inheritance tax in the Philippines?

How Can I Avoid Estate Tax in the Philippines?

- Sell your assets. You can sell your assets during your lifetime to your intended heirs or beneficiaries.

- Turnover to your heirs. You can also turn over your assets to your beneficiaries while you’re still living.

- Get insurance.

Can you transfer an estate tax exemption to a spouse?

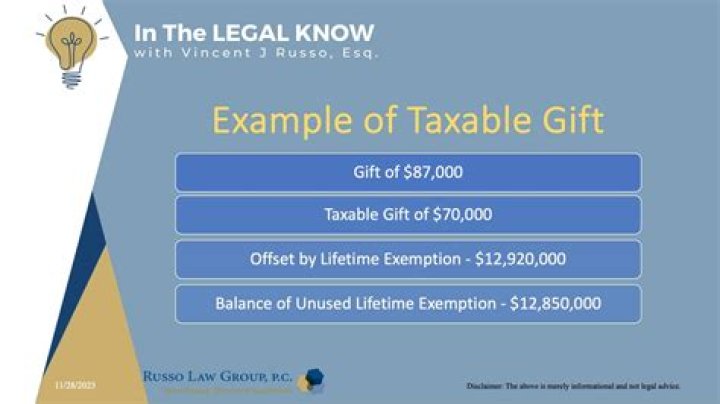

Importantly, the estate tax exemption is portable. Individuals can transfer the unused portion of their exemption to a spouse. For example, if an individual’s estate is worth $5 million, he or she could give $6.4 million of the exemption to his or her spouse.

Can a transfer of property be taxed as a gift?

Not all transfers of property are taxable for federal gift tax purposes. You can give as much as you want to your spouse without incurring the tax, barring a few exceptions. Four other types of transfers aren’t considered gifts for federal gift tax purposes, either:

How are estate, gift and generation skipping transfer taxed?

Wealth Transfer Taxes. The federal estate tax applies to the transfer of property at death. The gift tax applies to transfers made while a person is living. The generation-skipping transfer tax is an additional tax on a transfer of property that skips a generation. The United States has taxed the estates of deceased people since 1916.

How are Lifetime Transfers exempt from inheritance tax?

These lifetime transfers to individuals are called Potentially Exempt Transfers (PETs) and become totally exempt once the donor has survived for seven years from the date of the gift. You must have given up all rights to the asset for it to fall within the PET rules.