What are the licensing requirements to sell Variable Annuities? Applicant must be registered with the Financial Industry Regulatory Authority (FINRA). Applicant must have successfully completed the Securities Industry Essentials (SIE) exam; and either the FINRA Series 6 or 7 examinations.

Which are required of the prospectus for a variable annuity contract?

A prospectus for a variable annuity contract: must provide full and fair disclosure. is required by the Securities Act of 1933.

How do I sell a variable annuity?

There are two ways to sell your variable annuity: surrendering it to the company you bought it from, and selling payments you are receiving to a third party. When you surrender your annuity, the insurance company will pay you the account value less any surrender charges.

Do variable annuities require a prospectus?

The new rule permits variable annuity and variable life insurance contracts to use a summary prospectus to provide disclosures to investors. A summary prospectus is a concise, reader-friendly summary of key facts about the contract.

What are the different types of variable annuities?

A variable annuity is a type of annuity contract that allows for the accumulation and disbursement of capital on a tax-deferred basis (such as interest ).

What do you get for selling a variable annuity?

Profit from the mortality and expense risk charge is sometimes used to pay the insurer’s costs of selling the variable annuity, such as a commission paid to your financial professional for selling the variable annuity to you.” Administrative fees: “The insurer may deduct charges to cover record-keeping and other administrative expenses.

Is there a guaranteed return on a variable annuity?

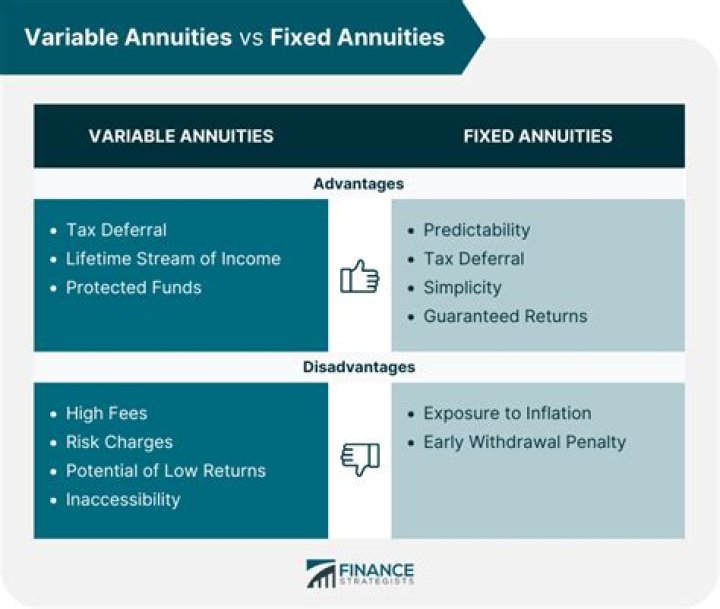

Most annuities will not allow the investor to withdraw funds from that account once the payout phase has commenced. Variable annuities were introduced in the 1950s as an alternative to fixed annuities, which offer a guaranteed return. Variable annuities do not guarantee a return.

How does a deferred variable annuity contract work?

With deferred annuities, you begin receiving income payments at a later date. If your variable annuity is structured also as an immediate annuity, there will be no accumulation phase. During this phase, your contract can increase in value.