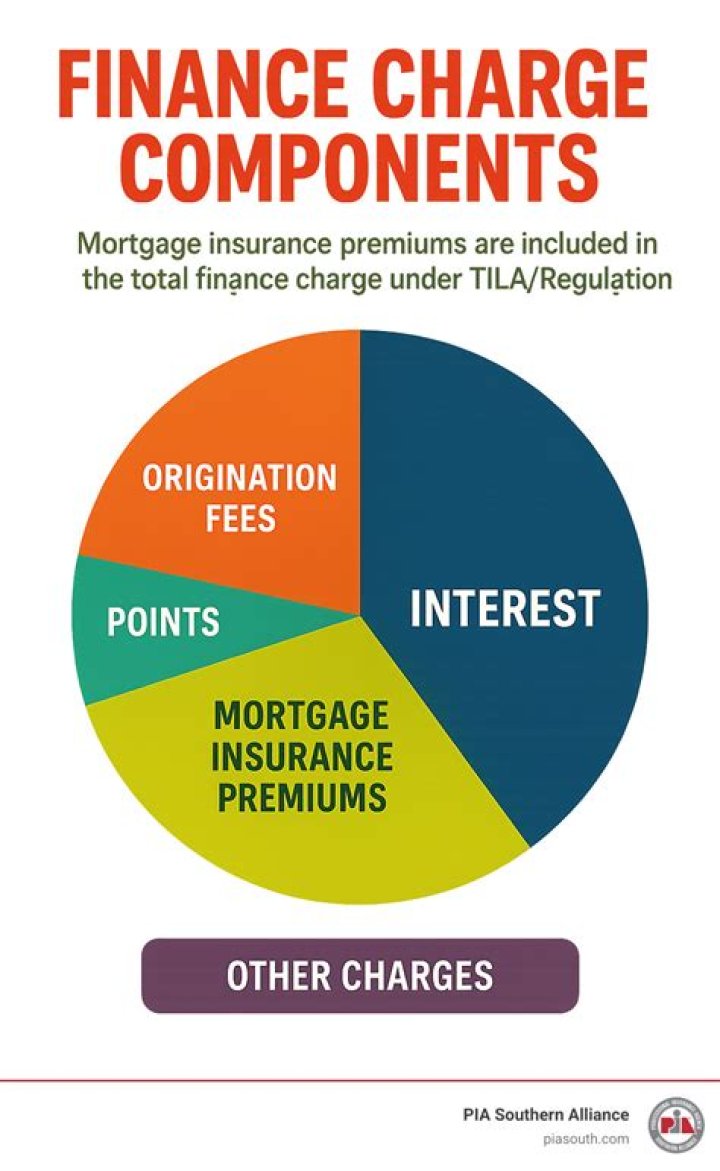

Examples of a finance charge include interest, points, and service or transaction fees. The TILA excludes certain costs from the finance charge, such as charges payable in a comparable cash transaction and fees paid to third-party closing agents (unless the creditor requires the services provided or retains the fee).

How many installment payments must be required before Truth in Lending disclosure is required?

When getting a new mortgage, you’ll receive truth-in-lending disclosures twice. The first is given to you when you apply for the mortgage. The second is given no less than three days before closing your escrow. It includes information on the cost of the loan and the interest rate you’ll pay.

When do you not apply finance charges to a customer?

If you choose not to apply finances charges to a customer because he or she has provided a good reason for the late payment, be sure the box in the Assess column is unchecked. If you want to change the finance charge due for a valid reason, you can type over the amount in the last column.

How much is a finance charge per day?

Finally, multiply your average daily balance by the DPR, and then multiply the result by the number of days in your billing cycle. With a 30-day billing cycle, a 0.055% DPR and a $1,200 average daily balance, your finance charge would be $19.80.

What are finance charges and why do they matter?

According to current regulations within the Truth in Lending Act, a “finance charge is the cost of consumer credit as a dollar amount. It includes any charge payable directly or indirectly by the consumer and imposed directly or indirectly by the creditor as an incident to or a condition of the extension of credit.

When do you pay a finance charge on a credit card?

If you don’t pay your balance in full by the due date each month and there is no promotional 0% APR period, you will incur a finance charge based on your card’s APR and the remaining balance. Best Low-Interest Credit Cards. ]