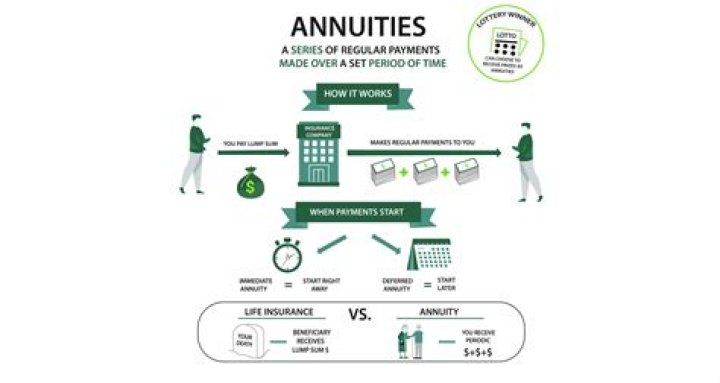

A deferred annuity is a contract with an insurance company that promises to pay the owner a regular income, or a lump sum, at some future date. Investors often use deferred annuities to supplement their other retirement income, such as Social Security.

What is the benefit of a deferred annuity?

The advantages of a deferred annuity An annuity allows you to save on a tax-deferred basis, meaning that earnings in the account are not taxed until they’re withdrawn. And if you contribute to the account with after-tax money, any of your contributions come out with no additional income tax liability.

What is a deferred annuity payment?

A deferred payment annuity is an insurance product that provides the buyer with future payments rather than an immediate stream of income. These annuities offer tax-deferred growth at fixed- or variable rates of return, just like regular annuities. Income can be received monthly, quarterly, annually, or in a lump sum.

Do you pay taxes on a deferred annuity?

Annuities are tax deferred. What this means is taxes are not due until you receive income payments from your annuity. Withdrawals and lump sum distributions from an annuity are taxed as ordinary income. They do not receive the benefit of being taxed as capital gains.

Which is the best definition of a deferred annuity?

Deferred Annuity Defined. A deferred annuity is a long-term investment in which you invest a sum of money, then receive payments several years down the line after the initial sum has accrued interest.

Do you have to pay taxes on deferred annuity?

Deferred annuities work a lot like the individual retirement accounts (IRAs) and 401 (k)s you’re probably more familiar with. So long as your money is in the deferred annuity, you don’t owe income taxes on your gains.

Do you get a commission on a deferred annuity?

Editorial Note: Forbes Advisor may earn a commission on sales made from partner links on this page, but that doesn’t affect our editors’ opinions or evaluations. A deferred annuity is an insurance contract that generates income for retirement.

Do you need a financial advisor for a deferred annuity?

Deferred annuity contracts can be complex, especially with variable and fixed index annuities. Because of the nuances surrounding fees, guarantees and investment terms, you may want to consult with a trusted financial advisor before making an annuity purchase. A deferred annuity can make sense if you’re in the years approaching retirement.