It’s a fundamental economic principle that when supply exceeds demand for a good or service, prices fall. If there is a decrease in supply of goods and services while demand remains the same, prices tend to rise to a higher equilibrium price and a lower quantity of goods and services.

What happens when supply increases and demand decreases?

A decrease in demand and an increase in supply will cause a fall in equilibrium price, but the effect on equilibrium quantity cannot be determined. For any quantity, consumers now place a lower value on the good, and producers are willing to accept a lower price; therefore, price will fall.

Who came up with supply and demand?

Alfred Marshall After Smith’s 1776 publication, the field of economics developed rapidly, and refinements were to the supply and demand law. In 1890, Alfred Marshall’s Principles of Economics developed a supply-and-demand curve that is still used to demonstrate the point at which the market is in equilibrium.

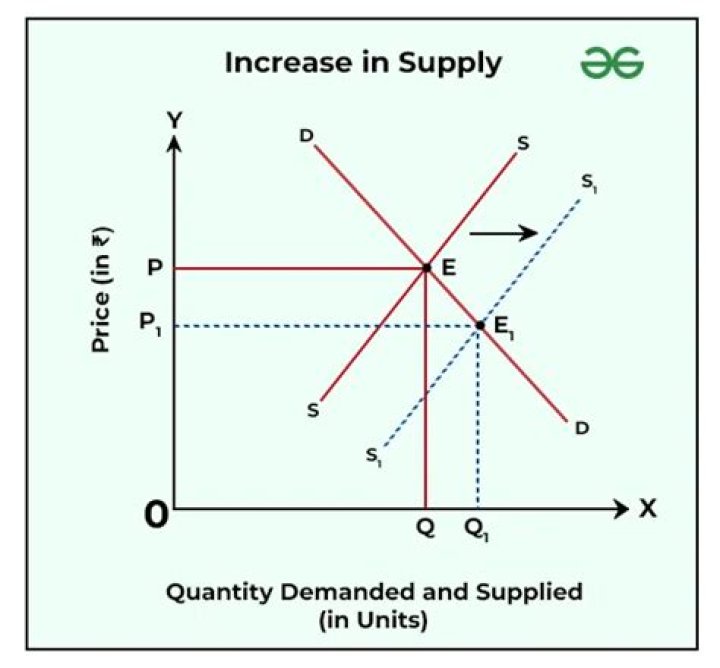

What happens when demand and supply rise at the same time?

At the same time, supply will fall. b. Price will rise. At the same time, supply and demand will fall. c. Price and supply will fall. At the same time, demand will rise. d. Price will fall. At the same time, demand and supply will rise.

What makes the quantity supplied and the price go up?

The quantity supplied and the price both go up. c. Shortage makes the good difficult to obtain. d. Excess supply makes the good easy to obtain. d. In response to rising car traffic, demand for bicycles has increased. The new equilibrium point will show a. more bicycles sold, but at a higher price.

Why do fads often lead to shortages, at least in the short term?

Why do fads often lead to shortages, at least in the short term? a. Buyers and sellers are unable to agree on a price for the good. b. Laws prevent stores from responding to excess demand in time to prevent a shortage. c. Manufacturers charge such high prices for the goods that stores are unwilling to pay.

Why does the government place price ceilings on some essential goods?

Why does a government place price ceilings, such as rent control, on some “essential” goods? In 1971 the American economy was suffering from a rapid increase in the cost of living. To combat this trend, the government temporarily froze all wages and prices. This action by the government is an example of