The biggest risk of using your car as collateral is that if you default on the loan, your bank or lender can take possession of your vehicle to help pay for part or all of your owed debt. Fees might also apply.

Do you need income for a secured loan?

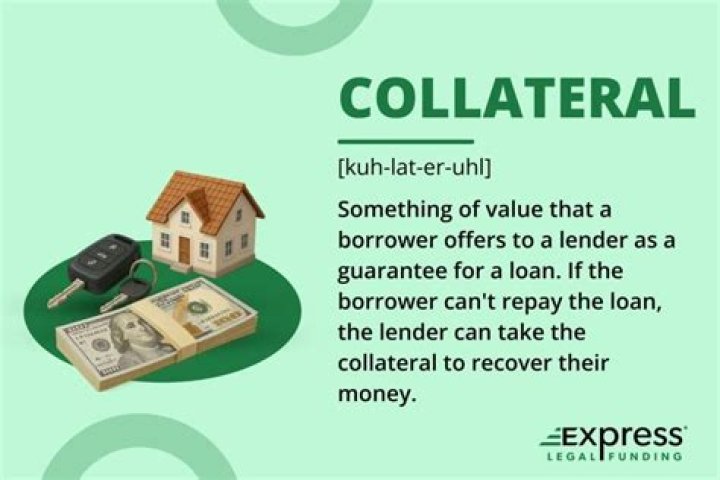

Secured loans Qualifying: Secured personal loans can be easier to qualify for than unsecured loans. A lender considers your credit score, history, income and debts, but adding a savings account or vehicle to the application to secure the loan can give lenders more confidence to lend to you.

Can a lender Sue you after a car is repossessed?

Perhaps the worst thing about having your car repossessed is that even after your vehicle is gone, your lender may not be done with you. In some cases, lenders may file lawsuits against borrowers to recoup what they’re owed. In this blog post, we’ll look at what’s involved with being sued after a car repossession.

Can a car be repossessed if you have security interest?

Every state has its own rules regarding repossession, but having a security interest generally means your lender can repossess the car without notice if you default on the loan. Many things can constitute a default, but the most common reasons are not making timely loan payments or not having car insurance.

What to do if secured creditors seize your car?

This means that if you stop making the payments for the car, and if the secured creditors seizes the car for non-payment, they cannot then come after you for any shortfall. The best bet is to sell the car if it can be sold for more than the debt so you can pay it off in full and get out of your financial obligation. cheap hair extensions

Can a judgment creditor take my car away?

The short answer to the question, “Can a judgment creditor take my car?” is “Maybe.” Generally, creditors will only take a vehicle if your car has value. A car with value can be beneficial to a creditor, as they can sell it and use that money to pay off the debt you owe. If a car has little value, creditors won’t go through the trouble.