Most retirement accounts, including the money in your 401k account, are fully protected from creditors when you file for bankruptcy. Because federal law protects these accounts from creditors and the bankruptcy trustee, cashing in a 401(k) to deal with debt is almost always a bad idea.

Does 401k distribution count as adjusted gross income?

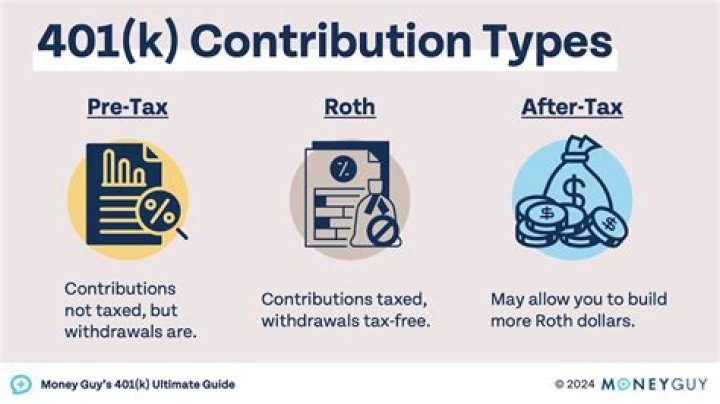

Traditional 401(k) contributions effectively reduce both adjusted gross income (AGI) and modified adjusted gross income (MAGI). A Roth 401(k), similarly to a Roth IRA, is funded through after-tax dollars and offers no immediate tax deduction.

Can I cash out my 401k while in Chapter 13?

Money saved in a 401k is “exempt” in bankruptcy and cannot be taken by the bankruptcy trustee. Withdrawing from a 401k in a Chapter 13 would have to be approved by the court because the debtor must commit all of her disposable monthly income to the Chapter 13 plan.

Is a 401k withdrawal considered income for a bankruptcy?

401 (k) is income and must be included in the Means Test. If that bring you over the limit you can file a Rebuttal of the Presumption. An experience Bankruptcy lawyer knows how to best handle such a situation.

Is the 401k protected in a bankruptcy case?

Your 401K is usually protected during bankruptcy although there are things you can do to put it at risk Ready for some good news? Retirement accounts are almost always protected in a bankruptcy case.

Is it bad faith to withdraw money from 401k?

No, people spend their money and run out of it all the time- whether it was from general savings, a 401k withdrawal or just regular monthly income. Running out of money is usually why people file bankruptcy, and there is no bad faith in filing bankruptcy for this reason.

Do you have to report 401k withdrawals as income?

When you reach retirement age, it’s time to start withdrawals from retirement savings plans that have been accumulating dollars over the decades. And yes, 401 (k) withdrawals count as income and must be reported to the Internal Revenue Service (IRS). 1 Starting at age 59½, retirement savers can start accessing their accounts without penalty.