In 2020, the IRS allows all taxpayers to deduct their total qualified unreimbursed medical care expenses that exceed 7.5% of their adjusted gross income if the taxpayer uses IRS Schedule A to itemize their deductions.

What is an allowed expense that can be deducted from adjusted gross income?

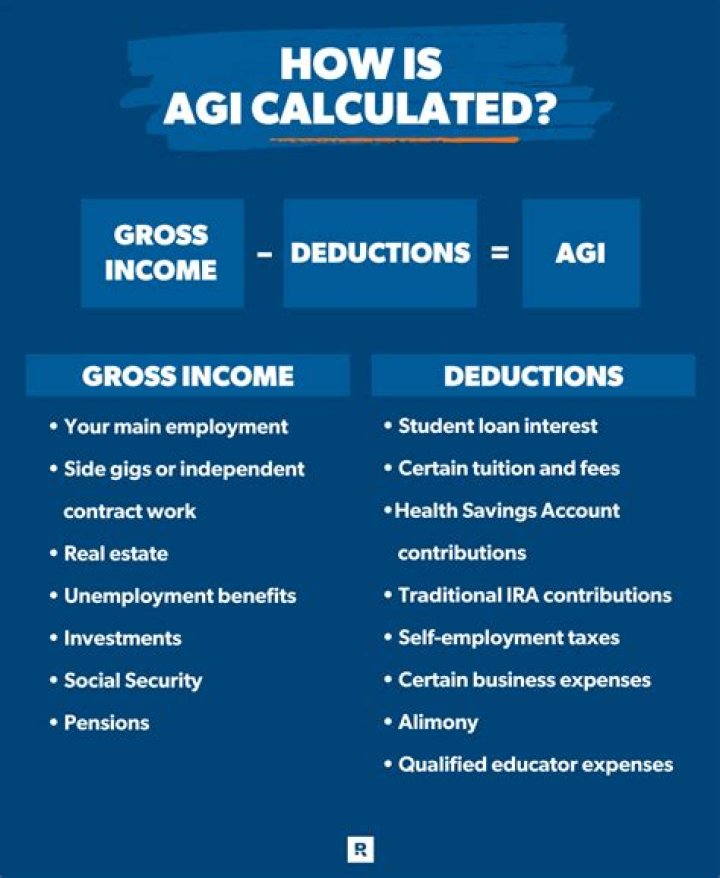

Several self-employment costs, such as retirement plan contributions, health insurance premiums, and half the self-employment tax reported on Schedule SE. Savings withdrawal penalty amounts. Student loan interest. Tuition and fees educational expenses.

What is subtracted from gross income to total income?

Subtract what is owed If your employer takes out taxes, you will find the total deductions on your pay stubs. Next, subtract taxes from your income to determine your net annual income. To finish with the same example: You determined that your gross income was $52,000.

How is gross income subtracted from taxable income?

Deductions are subtracted from gross income to arrive at your amount of taxable income. Gross income is all income from all sources that isn’t specifically tax-exempt under the Internal Revenue Code.

What kind of deductions can you take on gross income?

One of the first deductions from gross income is the appropriate personal exemption for an individual and his spouse and dependents. In addition to the personal exemption, taxpayers can take further deductions, either in the form of a standard deduction or by itemizing.

What happens when you subtract standard deduction from AGI?

You can then subtract either the standard deduction or the total of your itemized deductions from your AGI. 4 The result tells is your taxable income, the figure that’s used to calculate your federal income tax liability—how much you owe the IRS or the amount of a tax refund you can expect.

Where does adjusted gross income go on the new tax form?

On the new form, it will go on line 11 after you do the Schedule 2 calculations. As you do now, this could be as simple as looking at the IRS-provided tax table or going through worksheets depending on the tax treatment of your types of income. All tax credits are better than tax deductions because they reduce your tax bill dollar-for-dollar.