It is possible to use your home equity to take out a loan for a car, and you may get a better interest rate on your loan by taking that route. Before you move forward, though, consider the risks of using your home as collateral and the drawbacks of choosing a longer loan.

Can a home equity loan be used for?

Some lenders may impose restrictions — for instance, some will not let you use the funds to pay for college tuition — but in general, home equity loans can be used for any legal purpose. Taking out a home equity loan to buy a car is a fairly simple process.

Which is better a home equity loan or a credit card?

Low rates: Home equity loans typically have a lower interest rate (usually quoted as APR) than unsecured loans such as credit cards and personal loans. A low rate can help keep borrowing costs low, but closing costs may offset low rates.

Can you get a second mortgage with home equity?

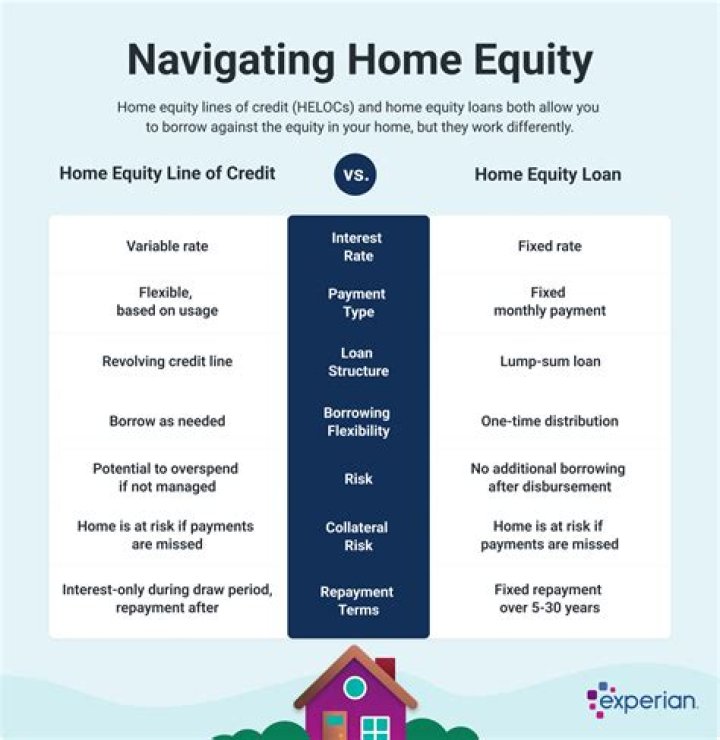

Second Mortgage (Home Equity Loan): Also referred to as a fixed-rate home equity loan, second mortgages are lump-sum payments that have set terms for repayment. These usually carry fixed rates and are paid back in full by the end of the loan term, although interest-only home equity loans and balloon payments do exist.

Where can I get a loan to buy a car?

Most often this is either through the dealership, a bank, or an online lender. While most lenders charge a high interest rate when taking out a car loan, you do have another option. Using the home equity you have built up in your house after many years of making payments, you can finance a new or used vehicle.

How does buying a car affect my home loan in process?

However, if you are going through the process of applying for a mortgage and closing on a home, you may want to reconsider buying a new car until after the deal is finalized. If you feel that you must purchase a car before closing day, check with your mortgage broker or loan officer for advice first. You could be risking your home loan.