Yes, You Can Still Refinance While Unemployed You can refinance a mortgage if you’re unemployed, though there are additional challenges. Unfortunately, lenders often won’t accept unemployment income as proof of income for your loan. So, while refinancing during unemployment is difficult, it’s not entirely impossible.

Why would a company refinance?

Corporate refinancing is often done to improve a company’s financial position. Through refinancing, a company can receive more favorable interest rates, improve their credit quality, and secure more favorable financing options. It can also be done while a company is in distress with the help of debt restructuring.

What happens to loan if company goes bust?

As an asset, the Administrators will look to the company’s assets to try and get as much money as they can to pay the now defunct company’s creditors. In all probability, the loan you owe will be sold onto another agency, or lender, to be bought and collected.

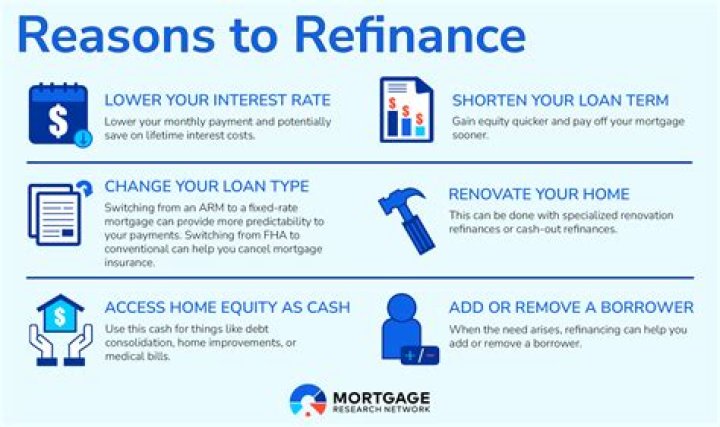

What happens when you refinance debt?

Refinancing debt results in lower monthly payments, which in turn frees up cash that can be utilized for other needs. A company can refinance its debt by replacing its current debt with a lower interest rate debt. Issuing new equity to pay down the debt load is another method of refinancing.

Can I close my Ltd company with a bounce back loan?

If you wish to close a company, and you took a Bounce Back Loan, it is still possible to eradicate the debt and close the limited company.

Are bounce back loans personally liable?

Can directors be personally liable to repay their company’s Bounce Back Loan? The short answer is no. Bounce Back Loans come with no personal guarantees. This means that in normal circumstances a director’s personal assets are not at risk if their company cannot repay its Bounce Back Loan.

What happens if a company does not go into receivership?

Receivership can occur even if a company does not go into bankruptcy. In cases where the Receiver will be appointed over a majority of accounts receivable, inventory and other property, the secured creditor must provide a minimum 10-day notice of intent. During this 10-day period, an interim Receiver may be appointed.

When does a receivership of a mortgage company end?

Receivership ends when the receiver has recovered the amount of money due to the mortgagee that appointed them. If you’re concerned about your rights as a mortgagee or mortgagor, and would like to find out more about the process and procedure of receivership, feel free to contact us today for a free consultation.

When to make payments to creditors in a receivership?

A. Receivers will generally make payments to creditors after realizing upon the Company’s assets and considering whether there may be surplus funds available after taking into account the current and anticipated expenses of administering the receivership, deemed trusts, statutory liens, and prior ranking claims.

Which is the best definition of a receivership?

What is ‘Receivership’. Receivership is a process in which a legally appointed receiver acts as custodian of a company’s assets or business operations, as with bankruptcies.