If you stop paying on a loan, you eventually default on that loan. The result: You’ll owe more money as penalties, fees, and interest charges build up on your account. Your credit scores will also fall.

Does a bank loan have to be paid back?

When you take out a loan you have a 14 day ‘cooling off’ period in which to cancel your agreement. Of course, you will have to repay all the money you have been loaned within 30 days, and the lender is legally allowed to charge you interest until they receive the loan back.

What happens if you do not repay a loan?

Defaulting on a loan is likely to lead to severe consequences, such as having your debt passed on to a collection agency, or being taken to court. If you have a loan secured with a car or your home, then it could be repossessed to recover the costs.

Why do you have to pay back a loan?

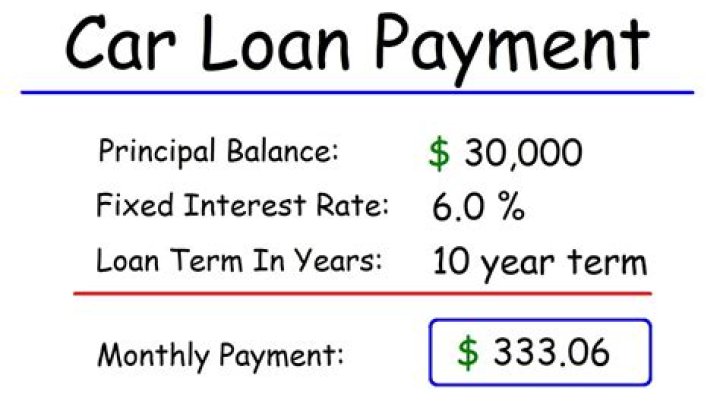

The mathematics of loan pay back. In most circumstances you would want to pay back your loan as it compounds the interest rate. Compounding means that the accrued interest rate is added to the principal and will accrue interest on its own in the next compounding period.

When do I have to pay back my SBA loan?

6-month deferment (you don’t have to start paying back the loan for 6 months—however, interest still accrues during this period) Note: as of June 5, 2020, payments are deferred until you receive approval from the SBA on your application for loan forgiveness, or 10 months after the end of your covered period.

How to calculate pay back on a student loan?

The loan calculator will output the pay back amount, the total payment over the entire loan term as well as the total accrued interest rate. Note that it doesn’t take into account fees for servicing the loan which would vary depending on the financial institution and your particular loan contract.

How much does it cost to pay back a 5% loan?

Initially a big proportion of the payments you make go into covering the interest rate which is quite high initially: for example, 5% interest on a $50,000 loan equals $208.33 during the first month of repaying your loan but it only equals $117.09 by the beginning of year 5 of repaying a 10-year loan.