With some lenders, you may be able to get the money you owe to the lender before they repossess the vehicle, but after the car title loan has defaulted. Some lenders may even send a notice of repossession to give you the chance to pay off the loan.

What happens if I can’t pay my car loan?

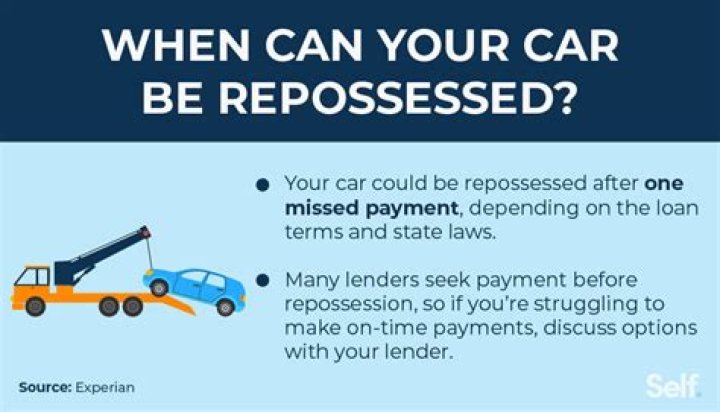

If you fall behind and can’t redeem the loan, it can repossess the car (take it back) after the first missed payment and sell it at auction (more about the repossession sale below). Here’s how it works. The lender will send someone out to tow your car to a storage facility.

How to pay a deficiency judgment after a repossession?

Negotiate a Payment Plan to Pay the Deficiency Even after a deficiency judgment is entered, your lender still may work out an agreeable payment plan with you. You can try to negotiate a payment by calling the lender or the lender’s attorney. Almost every lender’s attorney will take your call, and at least listen to payment offers that you make.

What happens when a car title loan is repossessed?

Once the borrower’s vehicle has been repossessed, the car title loan lender can choose to sell the car at an auction. Any of the money that they acquire from the auction will go towards the remaining balance of the loan.

When does a car company start the repo process?

Technically, a lender could initiate the car repossession process the day after you first default on a loan. Still, most lenders treat cases on a priority basis, going after second- and third-time defaulters first.

When to take action on a repo loan?

If you have no prior defaults on your payment plan and have always paid on time for three solid years, the lender is less likely to go the full nine yards in the weeks following your first default. On the other hand, the lender is more inclined to take immediate action if this is your second or third delinquency.